This update follows our previous note, Markets Continue to Climb a Wall of Worry. Despite headlines dominated by tariffs, slowing global growth, political risks, and uncertainty around inflation and interest rates, U.S. equity markets have remained remarkably resilient. The S&P 500 has posted five consecutive months of positive returns and set 19 new all-time highs in 2025 (as of August 28th). Yet this advance has been a rally many investors are reluctant to embrace. History reminds us that markets can often advance despite persistent risks, finding support in strong fundamentals.

What is powering this rally? A combination of solid corporate earnings, record investment in artificial intelligence (AI), a rebound in GDP growth, and the prospect of lower interest rates. At the same time, sentiment remains muted and liquidity abundant, a mix that has historically provided a favorable backdrop for markets.

In this blog, we review the key drivers behind the market’s momentum and what investors should expect as we head into the historically weaker September–October period.

Earnings Momentum Supports the Market

Corporate earnings continue to underpin market strength. With 98% of S&P 500 companies having reported Q2 results, 81% beat EPS estimates and 81% topped revenue forecasts, both well above historical averages. Reported results point to 11.9% year-over-year earnings growth, potentially the third straight quarter of double-digit increases, with revenues up 6.4% and margins improving to 12.8%.[1]

Looking forward, analysts are turning more optimistic. Analysts have raised EPS estimates for Q3 (+0.5%), and 2025 full-year EPS estimates are up 1.6% since June 30. For calendar year 2025, earnings are projected to grow 10.6%, followed by an even stronger 13.4% in 2026.[5]

These expectations highlight not only the strength of current results but also the adaptability of U.S. corporations. Even in the face of inflation, high interest rates, tariff risks, and policy challenges, companies continue to adjust and deliver growth.

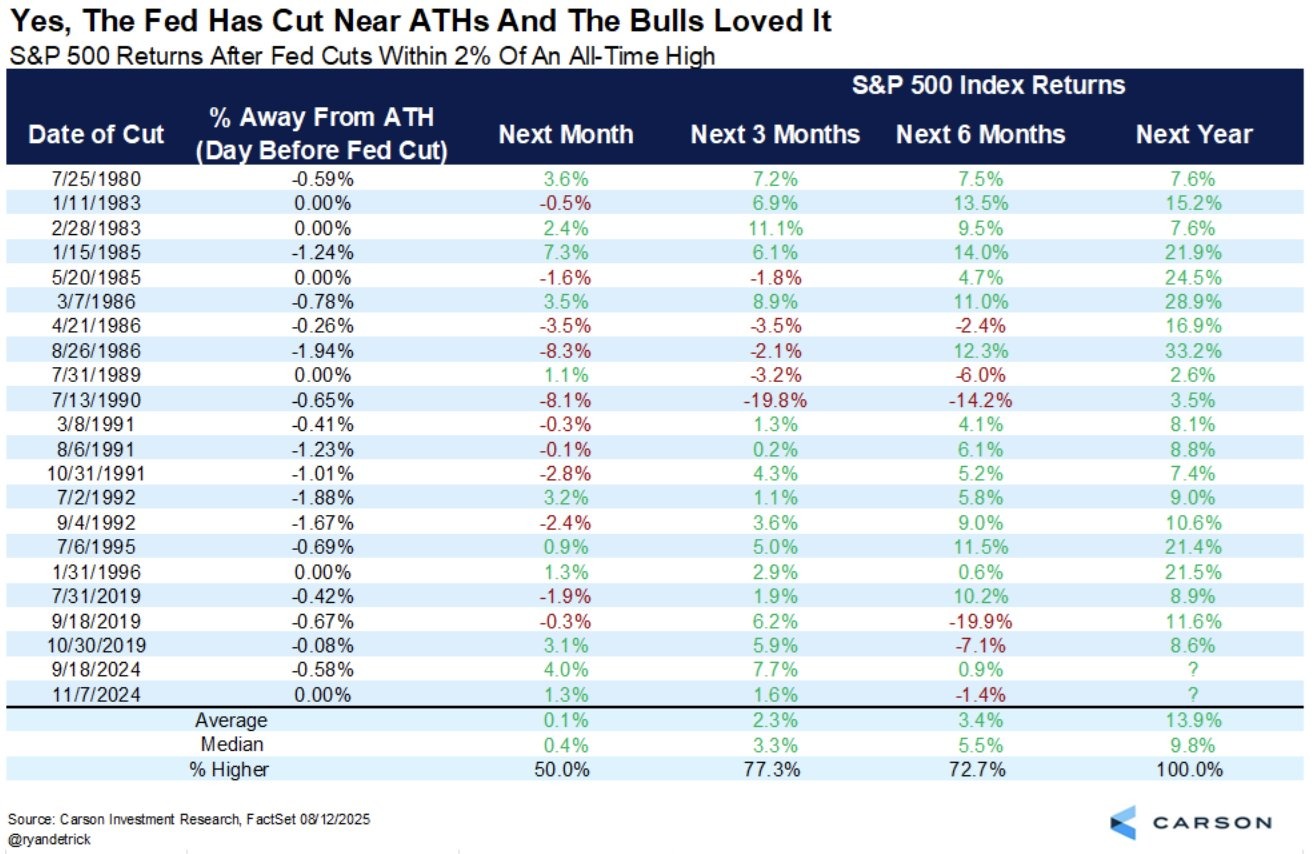

Fed Rate Cuts Provide a Bullish Tailwind

Beyond earnings, monetary policy is also shaping the backdrop for markets, with expectations for Fed rate cuts adding another layer of support. At the annual Jackson Hole Economic Policy Symposium in August, Fed Chair Jerome Powell noted that policy remains in “restrictive territory” and that shifting risks could soon justify rate cuts[6]. Markets are now pricing in two 25-basis-point cuts before year-end (as of September 2, 2025).

Lower rates tend to boost the economy by lowering borrowing costs for businesses, supporting consumer credit, and revitalizing housing activity. Importantly, these benefits also flow through to stronger corporate earnings.

History supports this constructive view. When the Fed has cut rates with the market within 2% of all-time highs, the S&P 500 has delivered positive returns over the next 12 months in every instance. On average, the index gained about 13.9%, with a 100% hit rate of positive outcomes.[7]

Table. Carson Research – Fed Rate Cuts when S&P 500 within 2% of High

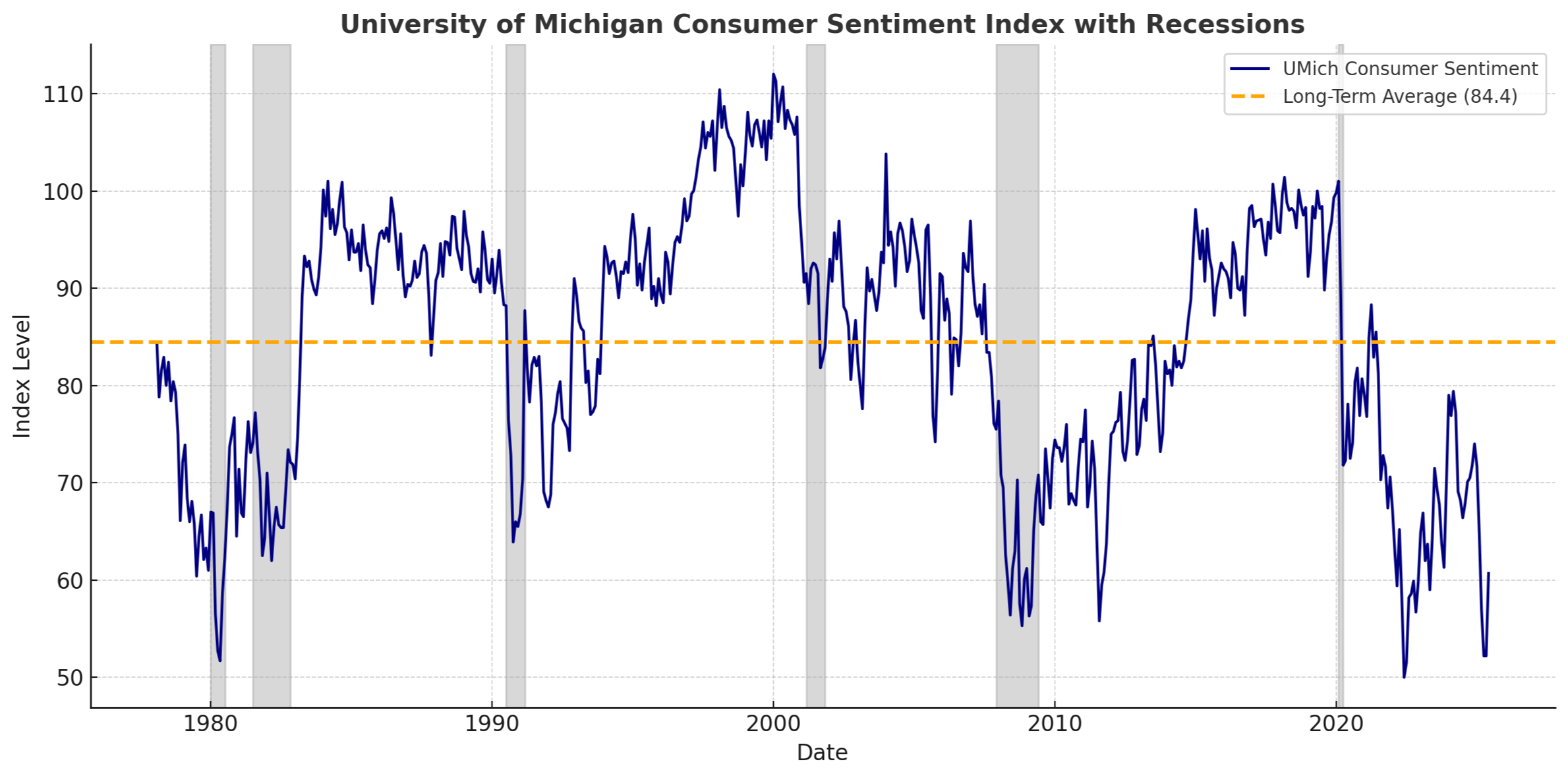

Subdued Sentiment and Confidence

While earnings and policy provide a strong foundation, investor sentiment tells a different story, one of caution rather than euphoria. The University of Michigan Consumer Sentiment Index is still well below its long-term average, signaling households are far from euphoric. Similarly, the AAII Investor Sentiment Survey most recently showed a bull–bear spread of –4.8%[8], meaning more investors identify as bearish than bullish. Historically, major market tops are uncommon when skepticism runs this high.

Table. University of Michigan Consumer Sentiment Index

Source: University of Michigan via FRED®

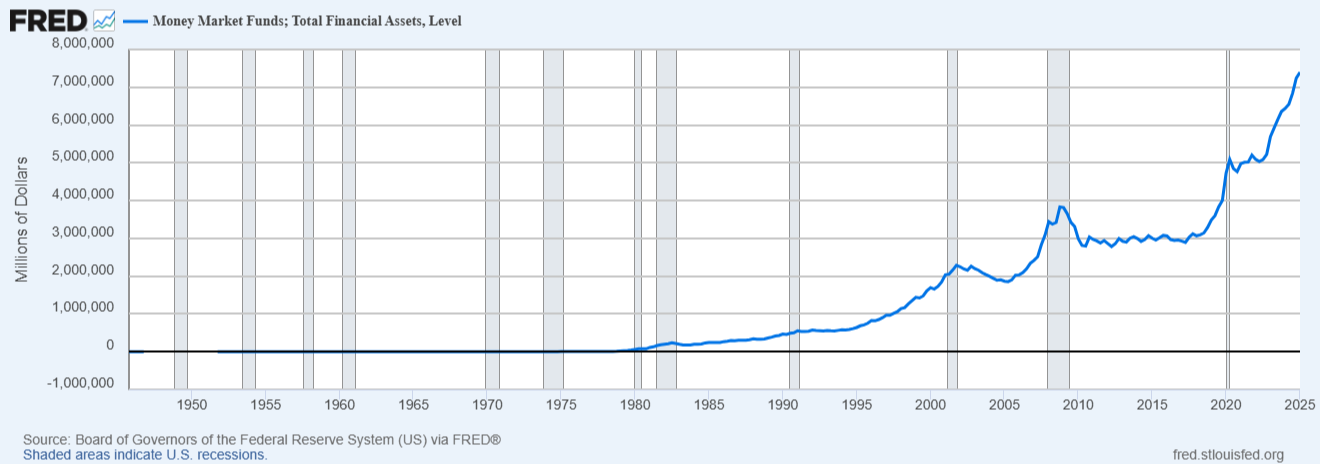

Meanwhile, liquidity remains abundant. Money market fund balances have climbed above $7 trillion, far above pre-pandemic levels. Private sector cash balances also sit at about 76% of GDP, compared with just 57% at the onset of past recessions[9]. This excess “dry powder” can act as a buffer and suggests that any significant pullback is likely to be met with buyers.

Table. Money Market Funds

What to Expect

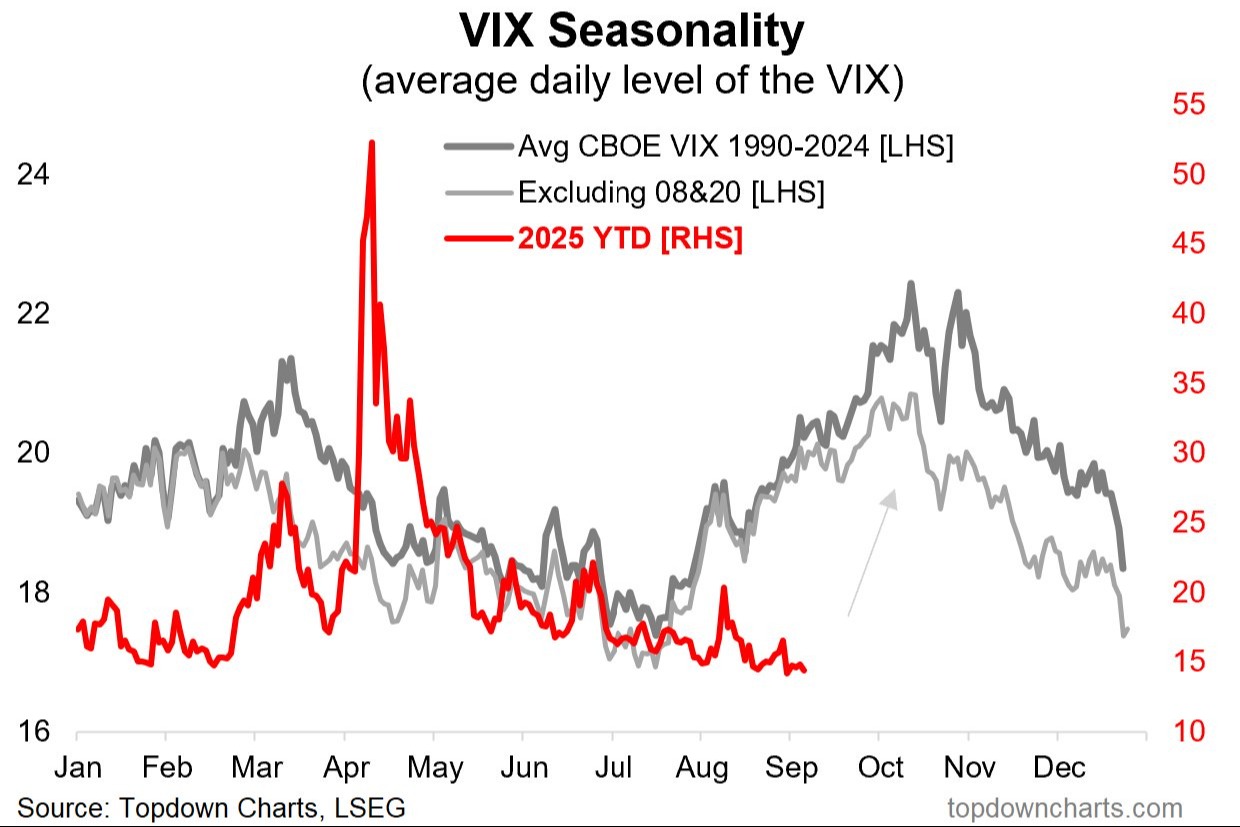

The cautious sentiment and ample liquidity come at a time when markets are entering a seasonally weaker period, making the economic backdrop even more important. As we move into September and October, this stretch has historically been one of the weakest periods for equity markets, with volatility often picking up during this seasonal window. The VIX (CBOE Volatility Index, often called Wall Street’s “fear gauge”) measures expected stock market volatility and tends to rise in these months. The VIX seasonality chart from Topdowncharts.com illustrates this trend, showing that volatility has historically spiked in the fall, with October often marking the highest levels[10].

Chart. VIX Seasonality Chart

The broader economic backdrop remains supportive. GDP rebounded strongly in Q2, revised upward to a 3.3% annualized growth rate following a temporary Q1 contraction that was largely driven by inventory distortions as companies rushed orders ahead of tariff changes. Looking ahead, the Atlanta Fed’s GDPNow model projects another solid quarter, with 3.0% growth expected in Q3 (as of September 2, 2025).

In addition to seasonal factors, several potential catalysts could usher in more volatility in the months ahead. We are monitoring developments in the labor market, budget negotiations, tariff discussions, and Federal Reserve policy decisions, all of which could create near-term uncertainty for investors.

Even if markets experience short-term turbulence in the coming months, the combination of steady growth, resilient earnings, and supportive policy should help the market remain on solid footing heading into the fourth quarter. We continue to believe that the longer-term trend is positive, and that equities can maintain their ability to grind higher in the fourth quarter despite seasonal headwinds.

Conclusion

Resilient earnings, strong investment in AI, and supportive policy shifts suggest the market rally rests on a solid foundation. While volatility is always part of investing, corporations have repeatedly adapted through challenges such as COVID-19 shutdowns, supply chain disruptions, inflation spike, historic rate-hike cycle, tariff pressures, and geopolitical risks. That resilience reinforces our confidence that markets can continue to perform and underscores the importance of staying focused on long-term goals rather than short-term swings.

Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly.

All investing involves risk including loss of principal. No strategy assures success or protects against loss.

The economic forecasts set forth in this material may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Stock investing includes risks, including fluctuating prices and loss of principal. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities.

[1] FactSet Research Systems Inc. (2025, August 29). Earnings Insight. Retrieved from https://insight.factset.com

[2] FactSet Research Systems Inc. (2025, August 29). Earnings Insight. Retrieved from https://insight.factset.com

[6] Reuters. “Powell Says Fed May Need to Cut Rates, Will Proceed Carefully.” August 22, 2025. https://www.reuters.com/markets/wealth/powell-says-fed-may-need-cut-rates-will-proceed-carefully-2025-08-22

[7] Ryan Detrick. “Will the Fed Really Cut Rates with Stocks near New Highs?” Carson Group Insights Blog, August 19, 2025. https://www.carsongroup.com/insights/blog/will-the-fed-really-cut-rates-with-stocks-near-new-highs/

[8] AAII. “AAII Sentiment Survey: Pessimism Pulls Back.” AAII Latest Commentary, August 28, 2025. https://www.aaii.com/latest/article/337536-aaii-sentiment-survey-pessimism-pulls-back

[9] Paulsen Perspectives. “Can We Have a Recession When…?” Paulsen Perspectives (Substack), [Publication Date]. https://paulsenperspectives.substack.com/p/can-we-have-a-recession-when

[10] Callum Thomas (@Callum_Thomas). X (formerly Twitter), August 29, 2025. https://x.com/Callum_Thomas/status/1961536644819099997