In early April, we wrote about the sharp market volatility triggered by the announcement of sweeping new tariffs from the Trump administration. At the time, we outlined key risks and four areas we were closely watching to gauge whether this policy shock would become a prolonged disruption or a passing storm.

Now, nearly two months later, we’re following up with a fresh perspective on how these factors have evolved — and why, despite ongoing uncertainty, we believe the market remains positioned to move forward.

A Recovery Driven by Policy Flexibility

After the initial sell-off in response to the tariff announcement, the S&P 500 has regained ground following news of tariff pauses and signs of policy flexibility from both the U.S. and key trading partners. Markets have responded positively to indications that the rollout may be more measured than initially feared. Countries including South Korea, India, and the EU have engaged in diplomatic discussions, and the staggered implementation timeline has allowed room for dialogue and adjustment.

Yet this rebound has been met with skepticism. The market’s climb could be described as one of the “most hated rallies,” driven not by euphoria but by resilience — a grind higher as investors reassess risk, reposition portfolios, and digest fast-moving headlines.

What We Were Watching — and Where Things Stand Now

In our April blog, we identified five key areas to monitor. Here’s how those themes have developed:

- Volatility as an Opportunity Signal

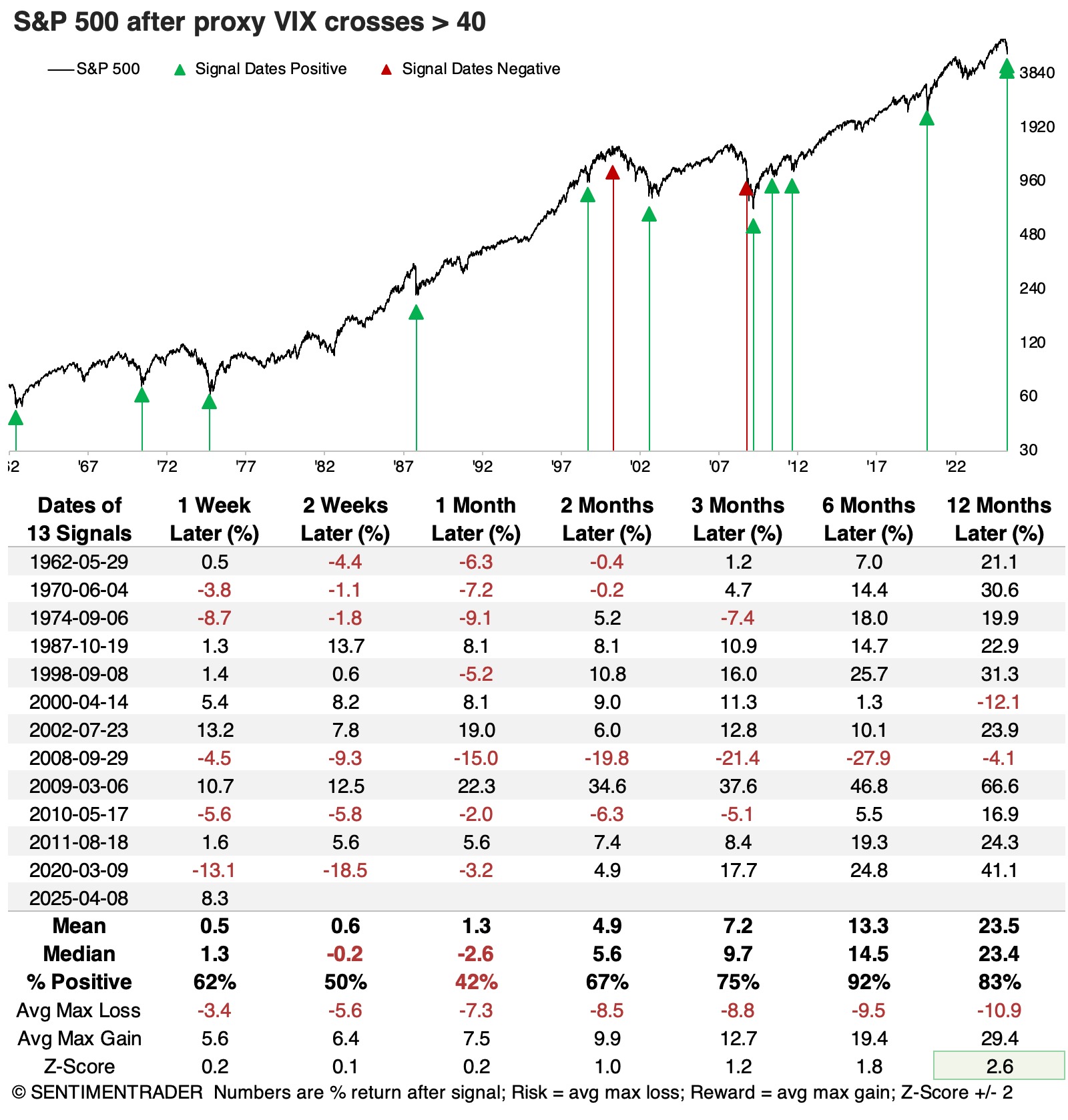

We highlighted that volatility — as measured by the VIX — had spiked sharply following the tariff announcement. Historically, such spikes have created opportunity, not just turbulence. Recent price action supports that view: on April 7, 2025, the VIX surged above 40 — a level rarely seen outside of major crises — signaling just how intense the uncertainty had become.

More importantly, when the VIX crosses this extreme threshold, historical data shows strong forward returns. The chart below from SentimentTrader illustrates S&P 500 performance following past instances when the VIX (or its proxy) exceeded 40.

Source: SentimentTrader

Across the 13 signals since 1962, the average 12-month return following a VIX spike above 40 was 23.5%, with 83% of outcomes positive. Even the 6-month and 3-month periods following these spikes produced double-digit average gains — well above historical averages[1].

This reinforces our broader view: volatility, while uncomfortable in the moment, often signals opportunity for patient investors — though it is important to note that past performance does not guarantee future results. It also explains why we continue to see recent market volatility as a reset, not a retreat.

Importantly, sentiment indicators that we follow continue to reflect a subdued investor landscape — another reason we view the recent rally as fundamentally healthy, not euphoric. The AAII Bull-Bear Sentiment Index continues to show that investors remain broadly bearish[2]. FINRA Margin Debt has not surged during the rebound, indicating a lack of excessive leverage in the market[3]. Finally, the May Bank of America Global Fund Manager Survey showed a decades low allocation to equities — further evidence that professional managers are not chasing this rally[4].

These sentiment indicators are good contrarian signals and provide further reasons why the market may be able to continue grinding higher. Unlike past market tops and major declines, today’s environment lacks the leverage and investor euphoria that often precede significant drawdowns.

- Corporate Credit Markets

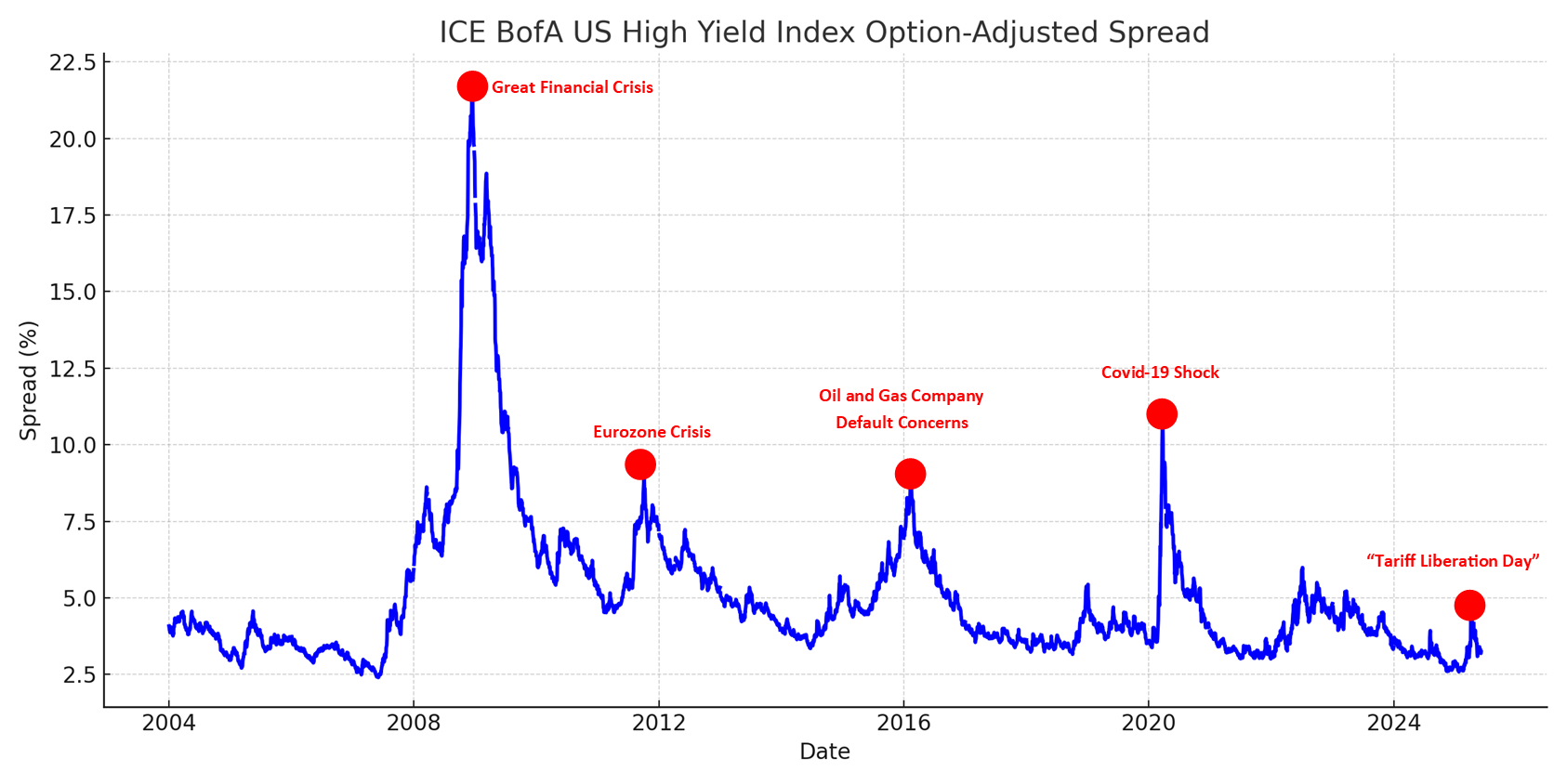

High-yield credit spreads offer a clear lens into investor sentiment during periods of market stress — and they’ve been notably well-behaved in the wake of the recent tariff-driven volatility.

As shown in the chart below, credit spreads never spiked to levels associated with prior periods of economic distress, such as the Global Financial Crisis (2008–2009), the Eurozone debt crisis (2011–2012), Oil and Gas Company Default Concerns (2015-2016), or the COVID-19 shock (2020). Even following the so-called “Tariff Liberation Day,” spreads only widened modestly and have since retreated — a strong signal of underlying market stability.

Chart. ICE BofA US High Yield Index Option-Adjusted Spread

Source: Ice Data Indices, LLC via FRED®

Credit markets are often seen as the canary in the coal mine — typically flashing warning signs before broader markets react. Their calm response suggests that investors in fixed income markets view the current environment as disruptive, but not systemically threatening. This reinforces our view that recent volatility is not being driven by fundamental credit concerns, and that recession risk remains low in the near term.

- Earnings Revisions

A key concern earlier this year was that companies would stop providing 2025 earnings guidance due to trade and economic uncertainty. That has not materialized. According to FactSet, of the 478 S&P 500 companies that reported Q1 2025 results, 259 (54%) issued full-year EPS guidance. Only 8 companies (3%) pulled or declined to update guidance — with most citing sector-specific issues.[5]

More telling, those maintaining guidance were nearly twice as likely to raise (64) than lower (37) their projections. This reinforces the message that corporate management teams remain confident in their outlooks — a key reason the S&P 500 has rebounded and continues to trade at 21.1x forward earnings, well above the 10-year average of 18.4x.[6]

U.S. businesses have navigated a gauntlet over the past five years — including the COVID-19 crisis, supply chain shocks, inflation spikes, and the fastest rate hike cycle in decades — and yet they’ve remained profitable and resilient. We believe they will continue to demonstrate this adaptability through current market turbulence.

- International Diplomacy

Encouraging signs have emerged. Some U.S. allies have indicated openness to trade discussions, and the U.S. administration has hinted at flexibility in enforcement and scope. The tone remains cautious, but the path forward now seems less confrontational than it did in early April.

- Ongoing Budget Negotiations

Another area we have been monitoring closely is the progress of ongoing U.S. budget negotiations. Fiscal policy can play an important role in shaping both economic momentum and market confidence, particularly in an environment already challenged by trade uncertainty.

In recent weeks, negotiations have advanced incrementally, with bipartisan discussions centered on finalizing discretionary spending levels and potential extensions of select stimulus-related provisions. While a significant new fiscal stimulus package is unlikely, a credible budget resolution would help reduce tail risks around a potential government shutdown — and provide further clarity for businesses and consumers.

Conversely, a protracted or contentious budget debate later this summer could reignite volatility, particularly if debt ceiling issues or spending cuts come into sharper focus. We will continue to monitor developments on this front, as the budget outcome could influence both market sentiment and the broader economic outlook heading into the second half of the year.

Recession Risk: Still Not Our Base Case

Despite the noise, our base case remains that the U.S. will avoid a recession in 2025. Key reasons include:

- Continued strength in the labor market and consumer spending

- Solid earnings and corporate balance sheets

- Improved consumer confidence from historic lows

- Easing inflation trends and the potential for multiple Fed rate cuts this year

- Stabilization in financial conditions and credit flows

We remain mindful of risks — particularly if trade tensions escalate — but believe the market is increasingly looking through the policy turbulence and focusing on the economic fundamentals.

Looking Ahead

Tariff headlines will continue to drive short-term market swings. But the past two months have demonstrated that investors are not abandoning the long-term story. The V-shaped rebound, though unloved, has been real — and has rewarded discipline and patience.

We will continue to monitor developments across trade policy, earnings, and economic conditions. In the meantime, staying diversified, thoughtfully allocated, and focused on the bigger picture remains the best strategy.

Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly.

All investing involves risk including loss of principal. No strategy assures success or protects against loss.

The economic forecasts set forth in this material may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

[1]SentimenTrader. A Top 5 Volatility Scenario.https://users.sentimentrader.com/users/sentimentedge/a-top-5-volatility-scenario

[2]American Association of Individual Investors (AAII). AAII Sentiment Survey.https://www.aaii.com/sentimentsurvey

[3]FINRA. Margin Statistics.https://www.finra.org/rules-guidance/key-topics/margin-accounts/margin-statistics

[4]UBS Asset Management. Macro Monthly: June 2025.https://www.ubs.com/us/en/assetmanagement/insights/market-updates/articles/2025-06-macro-monthly.html

[5]FactSet. Earnings Insight, May 23, 2025.https://advantage.factset.com/hubfs/Website/Resources%20Section/Research%20Desk/Earnings%20Insight/EarningsInsight_052325.pdf

[6]FactSet. Earnings Insight, May 23, 2025.https://advantage.factset.com/hubfs/Website/Resources%20Section/Research%20Desk/Earnings%20Insight/EarningsInsight_052325.pdf