After five consecutive months of positive returns, investors are beginning the fourth quarter with a healthy dose of optimism and a fair amount of debate. The past five months have delivered strong equity performance, with the S&P 500 advancing roughly 7.8 percent in the third quarter alone.[1] As we move through October, some renewed volatility has emerged, which is not uncommon for a historically volatile month.

With valuations elevated, earnings trending higher, and the federal government currently in a shutdown, investors have plenty to monitor as we enter the final stretch of the year. In this blog, we take a closer look at key themes including valuations, earnings strength, and policy developments surrounding the shutdown, and discuss how they may influence market direction as we approach year-end.

Valuations: Perspective and Context

Valuations often draw attention when markets rise, but they are best understood as a reflection of earnings strength and investor confidence rather than a timing signal. When valuations expand, it typically indicates optimism about future profits and economic stability. Markets do not decline because valuations are elevated. They decline when earnings expectations fall.

Earnings Growth Supporting Higher Valuations

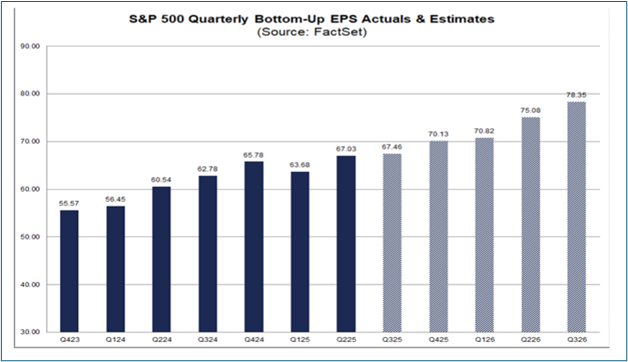

Corporate earnings continue to provide a solid foundation for recent market performance. For the first time since late 2021, Analysts raised earnings estimates for S&P 500 companies during a quarter rather than lowering them. This marks a meaningful shift in sentiment and reflects growing confidence in the resilience of U.S. companies despite persistent concerns about inflation and tariffs.[2]

Typically, analysts lower profit forecasts as a quarter progresses, but during the third quarter, S&P 500 earnings estimates rose from $67.32 to $67.41 per share. Though modest, this revision breaks a long-standing pattern of downward adjustments and reflects improving confidence in corporate profitability.

As shown below, analysts expect earnings growth to accelerate into 2025 and 2026. The chart highlights the steady climb in projected earnings per share (EPS) for the S&P 500, illustrating how forward-looking expectations helps support valuations.

Chart. FactSet Insights – S&P Quarterly Bottom-Up EPS Actuals & Estimates

Source: FactSet Research Systems Inc. (October 3, 2025). Earnings Insight. Retrieved from https://insight.factset.com. Copyright © 2025 FactSet Research Systems Inc. All rights reserved.

Valuations Are Only as Good as the Forecasts Behind Them

It is also worth noting that valuation methodologies are only as accurate as the assumptions that underlie them. Earnings predictions form the basis of most valuation models, and in 2025, those forecasts have proven to be too conservative. When companies outperform expectations, their profits rise, and the market’s valuation metrics look more attractive after the fact. In other words, the market may not be as expensive as it appears at first glance. When earnings grow faster than anticipated, prices can rise without stretching valuations. This dynamic helps explain how markets have sustained their rally even as headline P/E ratios remain above long-term averages.

Perspective: Then versus Now

Comparisons to the late 1990s dot-com era are understandable but imperfect. While stock valuations are above historical averages, they remain below the extremes of 2000. The S&P 500’s forward P/E ratio of roughly 22 compares with about 25 at the peak of the tech bubble. Meanwhile, corporate fundamentals are far stronger today. Modern market leaders are profitable, cash-generating companies that fund growth through internal cash flow rather than speculative borrowing.[3]

For additional comparison purposes, at the height of the dot-com era, Cisco Systems (one of the darlings of that period) traded up to roughly 210 times earnings. By contrast, Nvidia, one of today’s most closely watched AI-related companies, currently trades around 26.6 times earnings (as of September 9, 2025).[4] This contrast underscores how much more grounded valuations are today, with strong profitability and tangible earnings supporting prices rather than the speculative expectations that defined the late 1990s.

Combined with a Federal Reserve that appears to be moving toward easing policy, the current backdrop looks healthier and more sustainable than past speculative periods.

Monitoring Pockets of Euphoria

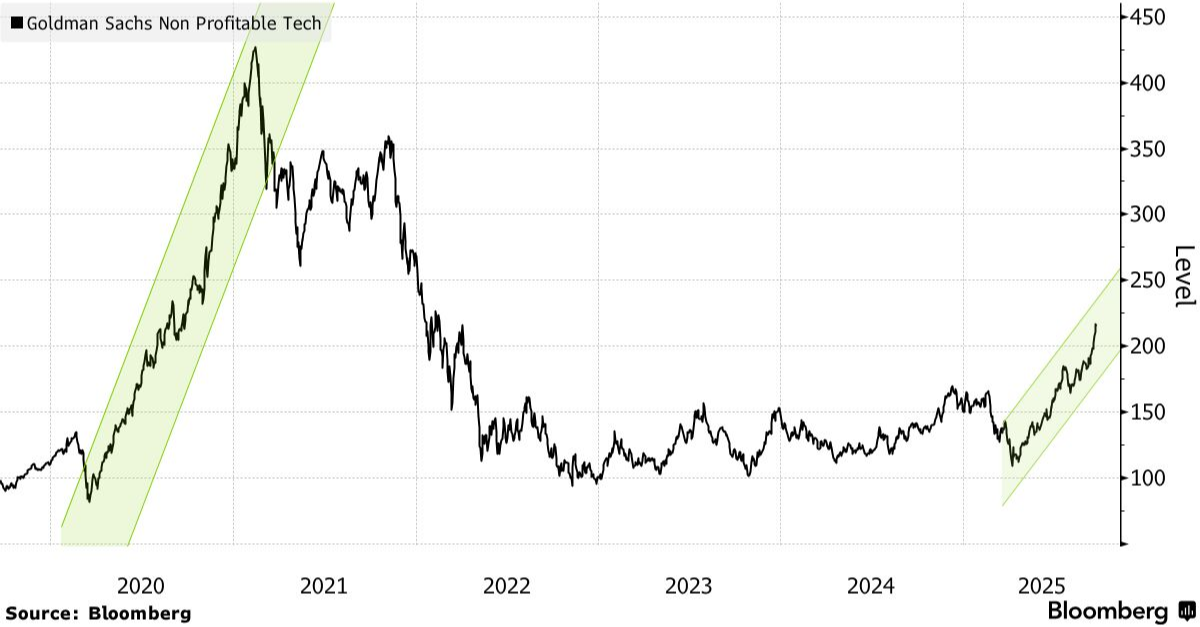

We are closely watching the growing enthusiasm across some of the more speculative corners of the market, particularly within innovative industries such as technology, industrials, and healthcare. One notable example is the Goldman Sachs Non-Profitable Technology Basket, which tracks companies in the tech sector that have yet to achieve profitability. According to recent Bloomberg data, this basket has surged more than doubled from its April low, benefiting from renewed investor optimism and expectations of easier monetary policy.[5]

While this type of rally can generate impressive short-term gains, it can also signal an increase in risk appetite. Importantly, even after the sharp rebound, the Goldman Sachs basket remains well below the peak levels reached in 2021, suggesting that investor enthusiasm has not yet reached the euphoric extremes of the prior cycle. Still, this is an area worth monitoring. Euphoria (when price seems to matter less than potential) typically develops in the later stages of a bull market.

Chart: Bloomberg Chart- Goldman Sachs Non-Profitable Tech Basket performance since 2020

Government Shutdown: Short-Term Noise, Limited Market Impact

While no one enjoys a government shutdown, history shows these events tend to have little lasting impact on financial markets. According to research from Zacks Investment Management, there have been more than 20 shutdowns since 1976, and none have caused a recession or triggered a bear market. In fact, the S&P 500 has gained an average of about 12 percent in the year following a shutdown, with several instances of positive returns even during the shutdown period itself.[6]

Shutdowns can delay economic data and create short-term uncertainty, but markets generally take them in stride. Essential services continue, and furloughed federal workers are typically paid retroactively, which helps spending recover quickly once the government reopens.

The key takeaway is that while shutdowns make headlines, they rarely alter the long-term trajectory of corporate earnings or market performance.

Other Risks We’re Watching

While the setup for the fourth quarter remains constructive, several risks bear watching:

- Inflation’s Second Wave: August CPI surprised to the upside. A renewed pickup in inflation could complicate the Fed’s expected easing path.

- Federal Reserve Policy and Dollar Stability: Confidence in independent Federal Reserve and a stable dollar remains vital to global market stability.

- Tech Concentration: The “Magnificent Seven” (Apple, Microsoft, Amazon, Alphabet, Meta, Nvidia, and Tesla) continue to drive a large share of market performance. Because of their outsized influence, any shift in investor sentiment toward these companies could introduce added volatility.

- Credit Spreads: We are watching credit spreads for signs of how fixed income markets respond to recent bankruptcy announcements. A noticeable widening would signal rising credit stress and tighter financial conditions.

- Creative Financing and Vendor Risk: Corporate financing practices, especially around AI and infrastructure, merit attention.

- Rising Long-Term Yields: Higher global yields could tighten financial conditions even as policy rates fall.

- Tariff Tensions: Renewed rhetoric between the U.S. and China in October could inject volatility if negotiations escalate.

Conclusion

After five months of positive momentum, the market enters the fourth quarter on solid footing. While October often brings volatility, it typically represents consolidation rather than reversal. Periodic pullbacks are normal and healthy in any market cycle. What matters most is the underlying cause of any pullback. Prolonged declines usually occur when earnings expectations weaken, and for now, profits continue to trend higher and support valuations.

Consumer sentiment also remains historically subdued, suggesting the market is far from euphoric. Low confidence has often coincided with favorable long-term outcomes, reinforcing the value of staying invested through short-term fluctuations.

With resilient earnings and the potential for a more supportive Fed, the outlook remains constructive even as we stay mindful of the risks ahead. As always, our focus remains on long-term discipline and the core drivers of portfolio growth including earnings, diversification, and thoughtful risk management.

Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly.

All investing involves risk including loss of principal. No strategy assures success or protects against loss.

The economic forecasts set forth in this material may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Stock investing includes risks, including fluctuating prices and loss of principal. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities.

[1] Detrick, R. (n.d.). A quarter for the history books — now what? Carson Group. Retrieved from https://www.carsongroup.com/insights/blog/a-quarter-for-the-history-books-now-what-2/

[2] Butters, J. (October 3, 2025). Earnings Insight. FactSet Research Systems. Retrieved from https://insight.factset.com. Copyright © 2025 FactSet Research Systems Inc. All rights reserved.

[3] Buchbinder, J. (n.d.). Fiber optics vs. data centers: Dotcom and AI comparisons. LPL Research. Retrieved from https://www.lpl.com/research/blog/fiber-optics-vs-data-centers-dotcom-and-ai-comparisons.html

[4] Lee, T. (2025, October 15). FSI First Word: US–China trade rhetoric heats up. 2025 proving to be worst year for fund managers in decades, setting up for performance chasing. Fundstrat Global Advisors.

[5] Vlastelica, R. (2025, September 24). “Frothy and Risky” Rally in Profitless Tech Grows as Fed Eases. Bloomberg. Retrieved from https://www.bloomberg.com/news/articles/2025-09-24/-frothy-and-risky-rally-in-profitless-tech-grows-as-fed-eases

[6] Zacks, M. (2025, October 10). Mitch on the Markets: Weekly Client Commentary. Zacks Investment Management. Retrieved from https://www.zacksim.com.