Many strategists have predicted small-cap stocks would be top performers in 2024 after seven straight years of underperforming large caps. However, as of the end of second quarter of 2024, the momentum in small caps has yet to fully materialize, with the S&P 500 up 14.8% year-to-date, while the Russell 2000 (a proxy for small-cap stocks) index has gained a modest 1.0%. While other markets are near or surpassed previous highs, the Russell 2000 still has some work to do to reach its November 2021 highs. Despite this slow start, we believe that small caps present a compelling risk-reward opportunity, bolstered by several economic, fundamental, and composition factors.

Economic Factors

From an economic standpoint, the U.S. economy has shown resilience. Despite an inverted yield curve persisting for two years, the economy has avoided a recession. The Atlanta Fed's GDP estimates for Q2 2024 is 2.0%[1], and the Philadelphia Fed's survey of professional forecasters indicates an improved near-term outlook. These forecasters now predict no recession in 2024, with GDP growth estimates of 2.5% for 2024 and 1.9% for 2025[2].

This stable economic environment is particularly favorable for small caps, which generate about 90% of their revenue domestically, compared to 60-65% for the S&P 500[3]. Additionally, small cap companies, which are often less profitable and more reliant on credit markets for growth and operations, stand to benefit from expected interest rate cuts. Easing financial conditions will likely alleviate some of the pressure these companies face.

While inflation reports earlier this year extended the timeline to eventual rate cuts, the potential easing of rates later in 2024 or early 2025 should create a more supportive environment for small caps.

Fundamental Factors

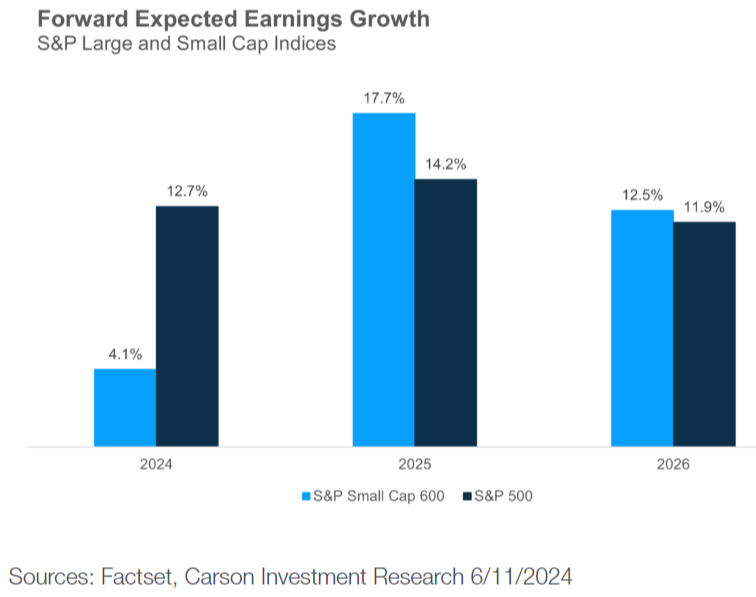

Valuations are closely tied to earnings, and with the number of unprofitable small-cap firms stabilizing, earnings growth for small caps is expected to accelerate in 2025 and 2026. The table below from Carson Investment Research illustrates the projected forward earnings for the S&P SmallCap 600 (a key small-cap stock index) compared to the S&P 500[4].

Additionally, Harbor Capital’s recent analysis of large-cap versus small-cap performance over the past 13 years reveals that large-cap stocks have outperformed primarily due to multiple expansion, or changes in P/E ratios. During this period, small-cap stocks experienced higher earnings growth, underscoring that their underlying fundamentals remain strong[5]. This suggests that the current price levels for small caps might be driven more by sentiment than by fundamental weaknesses. Sentiment can shift rapidly, and a positive change could serve as a significant catalyst for small-cap stocks.

Finally, current valuation metrics highlight a compelling opportunity in small caps. As of May 31, small caps were trading at a forward P/E ratio that is 73% of that of large caps, indicating a 27% valuation discount. This valuation discount is in the 18th percentile of the past 35 years, suggesting that small caps are trading at historically attractive levels. Historical trends show that such discounts often precede strong future performance, making small caps a promising asset class for investors seeking growth potential[6].

Composition Factors

Sector rotation could further enhance the appeal of small-cap stocks. In the first half of the year, technology has been a major driver of large-cap performance, with large-cap indices having a significant technology allocation of 33% compared to just 15% for small-cap indices. This surge in large-cap stocks, particularly within the tech sector, has been driven by investors' enthusiasm for AI-related opportunities. However, as market focus begins to shift toward sectors like Industrials and Financials, small-cap stocks, which have a greater emphasis on these areas, could become increasingly attractive for investors seeking to capitalize on these evolving trends.

Conclusion

Investing in small-cap stocks offers a range of promising opportunities for portfolio growth. With their attractive valuations, the potential for lower interest rates, improving technical trends, and the possibility of an earnings acceleration in 2025, small caps are well-positioned for the future. While predicting the exact timing of when small caps will lead the market is challenging, incorporating these equities into your investment strategy could provide significant benefits and diversification.

[1] Federal Reserve Bank of Atlanta. (2024, July 10). GDPNow. https://www.atlantafed.org/cqer/research/gdpnow

[2] Philadelphia Federal Reserve Bank, Research Department, Survey of Professional Forecasters, Second Quarter 2024 on May 10, 2024, www.philadelphiafed.org

[3] Temple, R. (2023, December 4). Small caps poised to make big moves? Lazard Asset Management. https://www.lazardassetmanagement.com/us/en_us/research-insights/investment-research/small-caps-big-moves#:~:text=Russell

[4] Carson Group. (2024, July 11). Small caps: Value trap or timely add? Carson Group. https://www.carsongroup.com/insights/blog/small-caps-value-trap-or-timely-add/

[5] Harbor Capital Advisors. (2024, July 10). Active edge: Can small caps regain their sizzle? Harbor Capital. https://www.harborcapital.com/insights/active-edge-can-small-caps-regain-their-sizzle-/

[6] Fang, D. (2024, June 19). Concerned about market concentration and lofty valuations? Consider small caps. CFA Institute. https://blogs.cfainstitute.org/investor/2024/06/19/concerned-about-market-concentration-and-lofty-valuations-consider-small-caps/

Disclosures

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly.

The prices of small cap stocks are generally more volatile than large cap stocks.

The Standard & Poor’s 500 Index is a capitalization weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The Russell 2000 Index is an unmanaged index generally representative of the 2,000 smallest companies in the Russell 3000 index, which represents approximately 10% of the total market capitalization of the Russell 3000 Index.

Dividend payments are not guaranteed and may be reduced or eliminated at any time by the company.

All investing involves risk including loss of principal. No strategy assures success or protects against loss. There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk.